Subprime Credit Card

A subprime credit card is a type of credit card designed for subprime borrowers. Unfortunately, subprime credit cards are far more restrictive than traditional credit cards, in order to protect the lender against the heightened risk of default that is generally associated with subprime borrowers. Typically, subprime credit cards will carry higher interest rates than regular cards, to reflect the higher expected default risk associated with subprime borrowers. Their interest rates are often higher than traditional credit cards and incorporate other provisions designed to reduce the lender's risk. Declaring bankruptcy has a dramatic negative effect on one's credit rating. Subprime credit cards are credit cards intended for borrowers with poor credit ratings.

What Is a Subprime Credit Card?

A subprime credit card is a type of credit card designed for subprime borrowers. They are offered both by major banks and by dedicated subprime lenders.

Typically, subprime credit cards will carry higher interest rates than regular cards, to reflect the higher expected default risk associated with subprime borrowers. Other measures, such as reduced credit limits and upfront deposits, are also frequently employed.

Understanding Subprime Credit Cards

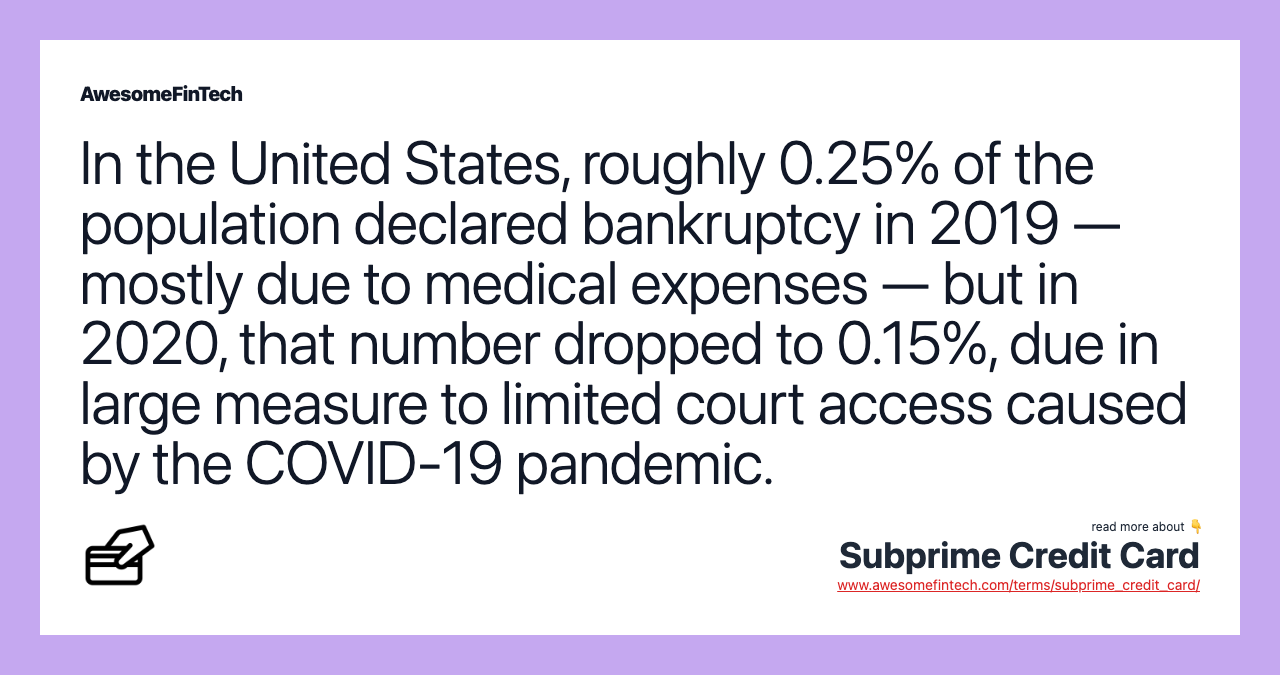

There are many reasons why a person might become labeled as a subprime borrower, the most dramatic of which being if they previously filed for bankruptcy protection. In 2019, approximately 750,000 people declared bankruptcy in the United States — or roughly 0.25% of the total population.

Among these cases, the single most common cause of bankruptcy was medical expenses, accounting for more than 60% of the total. Surprisingly, three-quarters of those who declared bankruptcy due to medical expenses — meaning, nearly 50% of all bankruptcies — were already covered by some form of health insurance. Other types of unexpected expenses, such as those associated with natural disasters or the sudden loss of a job, were also among the leading causes of bankruptcy in recent years.

Understandably, bankruptcy is recorded on an individual's credit report and has a severe negative effect on their overall credit score. Therefore, subprime borrowers may be unable to qualify for traditional credit cards, let alone cheaper forms of financing, such as personal lines of credit (LOCs). For such persons, subprime credit cards may be the only option available.

Unfortunately, subprime credit cards are far more restrictive than traditional credit cards, in order to protect the lender against the heightened risk of default that is generally associated with subprime borrowers. For example, subprime credit cards carry higher interest rates and account fees, with annual percentage rates (APRs) sometimes exceeding 30% per year. Other provisions, such as requiring the cardholder to provide an upfront security deposit, can further reduce the risk born by the lender.

In exchange for these terms, the borrower obtains the ability to slowly rebuild their credit score by regularly paying their credit card bills on time, while also benefiting from features such as rewards programs or cash-back rebates. On the other hand, subprime credit card users are at heightened risk of any future lapse in payments, since the cards' high APR could quickly cause interest payments to become unmanageable if the card's monthly balances are left unpaid for too long.

Real-World Example of a Subprime Credit Card

Subprime credit cards are available from numerous financial service providers. Current examples, as of July 2021, include the Credit One Bank Visa (V) card, the Bank of America (BAC)'s BankAmericard Secured Credit Card, and the Capital One Secured Mastercard (MA).

Some of these cards, such as the offerings by Capital One and Bank of America, require an upfront security deposit, typically between $100 and $300. Others, such as the Credit One Bank Visa card, are unsecured. Their interest rates are generally in the mid-20s, although their credit limits are often far lower than what is offered on regular credit cards.

Related terms:

Affinity Card

Offered through banks, affinity cards tied to nonprofit and charitable organizations can create a passive stream of donations. read more

Annual Percentage Rate (APR)

Annual Percentage Rate (APR) is the interest charged for borrowing that represents the actual yearly cost of the loan, expressed as a percentage. read more

Credit Card Debt

Credit card debt is a type of unsecured liability that is incurred through revolving credit card loans. It greatly affects your credit score. read more

Credit Scoring

Credit scoring generates a score that ranks, on a numerical scale, the credit riskiness of an individual or a small, owner-operated business. read more

Credit Card

Issued by a financial company giving the holder an option to borrow funds, credit cards charge interest and are primarily used for short-term financing. read more

Credit Report

A credit report is a detailed breakdown of an individual's credit history, provided by one of the three major credit bureaus. read more

Interest Rate , Formula, & Calculation

The interest rate is the amount lenders charge borrowers and is a percentage of the principal. It is also the amount earned from deposit accounts. read more

Line of Credit (LOC) , Types, & Examples

A line of credit (LOC) is an arrangement between a bank and a customer that establishes a preset borrowing limit that can be drawn on repeatedly. read more

Private Label Store Credit Card Defined

A private label credit card is a store-branded credit card that is intended for use at a specific store. It offers credit and sometimes special benefits at those stores. read more