Old-Age and Survivors Insurance (OASI) Trust Fund

The Old-Age and Survivors Insurance Trust Fund (OASI) is a U.S. Treasury account used to deposit tax receipts that fund Social Security benefits paid to retired workers, their surviving spouses, and eligible children. The Old-Age and Survivors Insurance Trust Fund (OASI) is a U.S. Treasury account used to deposit tax receipts that fund Social Security benefits paid to retired workers, their surviving spouses, and eligible children. Together, the OASI and DI Trust funds — known as Social Security — provide retirement, survivorship, and disability benefits to 65 million Americans, paying out more than $1 trillion each year. The combined OASI and DI trust funds held $2.9 trillion in 2020. The Old-Age and Survivors Insurance (OASI) Trust Fund is a Treasury account used to pay out Social Security benefits. The fund is managed by the Social Security Administration (SSA), which holds the authority to distribute OASI Trust Fund benefits to eligible parties.

What Is the Old-Age and Survivors Insurance (OASI) Trust Fund?

The Old-Age and Survivors Insurance Trust Fund (OASI) is a U.S. Treasury account used to deposit tax receipts that fund Social Security benefits paid to retired workers, their surviving spouses, and eligible children.

In other words, the OASI is the long name of Social Security. The fund is managed by the Social Security Administration (SSA), which holds the authority to distribute OASI Trust Fund benefits to eligible parties.

How the OASI Trust Fund Works

The Old-Age and Survivors Insurance Trust Fund was established on January 1, 1940, as part of the Social Security Act amendments of 1939. Payroll or employment taxes received under the Federal Insurance Contributions Act (FICA) and the Self-Employment Contributions Act (SECA) are deposited daily into the OASI Trust Fund held in a separate account at the U.S. Treasury.

The fund has automatic spending authority to pay monthly benefits and doesn’t need to make special requests to Congress to pay benefits. The OASI Trust Fund has been an important tool for supporting citizens, with a large part of the government’s expenditures being either Medicare or Social Security.

OASI Investments

The SSA invests the funds that are not required for current expenses. The OASI Trust Fund redeems or sells securities to make benefit payments or to pay other expenses. The money is invested in two types of interest-bearing Federal securities:

The interest earned from these investments is deposited into the OASI fund and used to make benefit payments.

OASI Board of Trustees

The fund's Board of Trustees consists of six members, two of whom are appointed by the President and confirmed by the Senate. The remaining four board member positions are held by Cabinet-level officials, including the:

Cost-of-Living Adjustments

Periodically, the Social Security Administration (SSA) increases the benefit based on an increase in the cost of living, which accounts for inflation or the pace of rising prices in the economy.

The SSA uses an inflation metric called the Consumer Price Index (CPI), which calculates the average prices of a basket of goods and services over a period of time. For example, in October 2020, the SSA decided to add a 1.3% cost of living adjustment (COLA) to the Social Security benefits.

OASI vs. OASDI

The benefits under OASI are actually part of a larger program called the Old-Age, Survivors, and Disability Insurance (OASDI) program. The OASDI includes the Disability Insurance (DI) Trust Fund designed to help people with permanent disabilities.

The Disability Insurance (DI) Trust Fund was established through the passage of the Social Security Act Amendments of 1956, and the program became effective on January 1, 1957. The DI operates in a similar manner to the Social Security benefits program (OASI). Funds from the disability trust are received through payroll taxes and invested in the same securities as the OASI. Both programs also have the same Board of Trustees.

Together, the OASI and DI Trust funds — known as Social Security — provide retirement, survivorship, and disability benefits to 65 million Americans, paying out more than $1 trillion each year.

Limitations of the OASI Trust Fund

The combined OASI and DI trust funds held $2.9 trillion in 2020. However, the 2021 annual report from the Social Security and Medicare Board of Trustees showed that the combined funds are projected to run out of money by 2034.

OASI Retirement and Survivorship Benefits

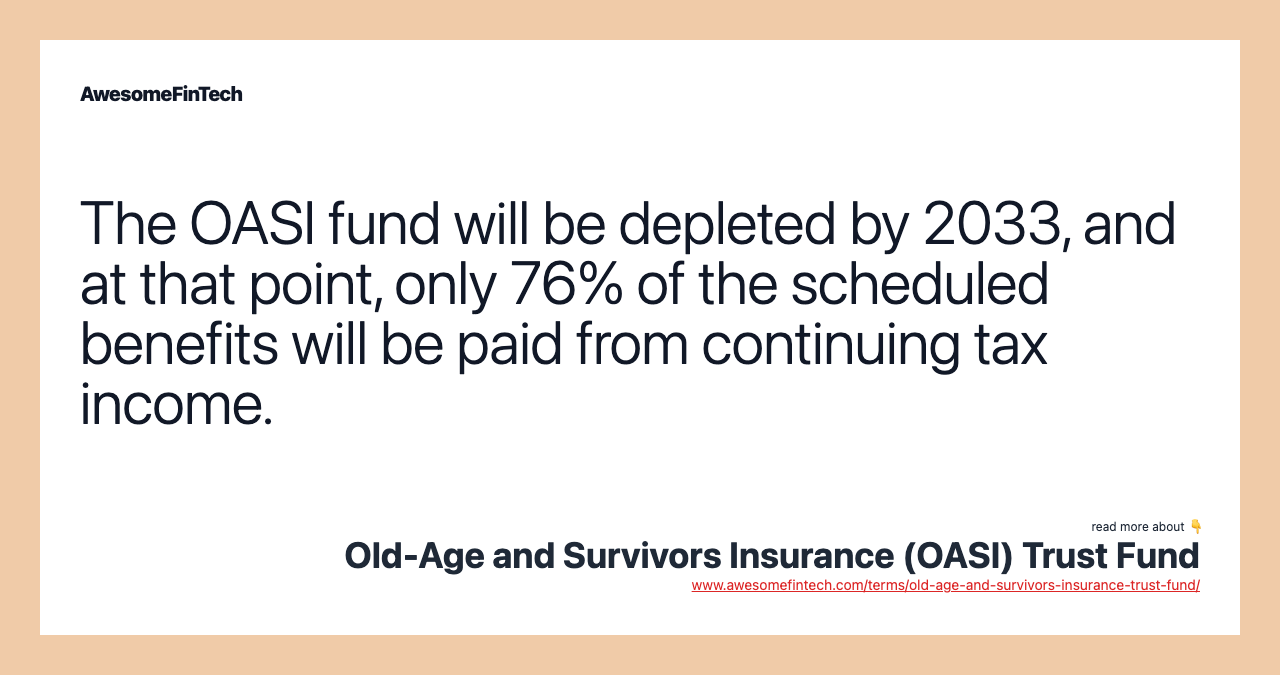

Unfortunately, the OASI will run out of money sooner. The report showed there's enough money to pay the scheduled retirement benefits until 2033. After that point, the funds will be depleted, and only 76% of the scheduled benefits will be able to be paid from continuing tax income.

Disability Benefits

The 2021 annual report also showed that the Disability Insurance (DI) Trust Fund is forecasted to have enough money to make scheduled benefit payments until 2057. After that, the DI fund's reserves will be exhausted, but continuing tax income is estimated to be enough to pay 91% of scheduled benefits.

Reasons for OASI's Financial Challenges

There are a number of financial challenges facing Social Security. The 2021 annual report noted that the coronavirus pandemic of 2020 had adversely affected the financial viability of the trust fund.

Another challenge facing Social Security is life expectancy. In 1940, a 65-year-old retiree had a life expectancy of another 14 years, while today, it's 20 years. Also, population growth has added to the financial challenges. For example, the number of Americans over the age of 65 today total 56 million, and by 2035, that number is expected to increase to 78 million.

As a result, there will be fewer workers paying into Social Security. For example, there are currently 2.8 workers for each Social Security beneficiary, and by 2035, the number of workers will be 2.3 per beneficiary. The U.S. Congress will likely need to make changes to replenish the fund, or future retirees may receive reduced benefits.

Related terms:

Consumer Price Index (CPI)

The Consumer Price Index (CPI) measures the average change in prices over time that consumers pay for a basket of goods and services. read more

Disability Insurance Trust Fund (DI)

The Disability Insurance Trust Fund (DI) is one of two Social Security Trusts which pays benefits to individuals incapable of gainful employment. read more

Federal Insurance Contributions Act (FICA)

The Federal Insurance Contributions Act (FICA) is a U.S payroll tax deducted to fund the Social Security and Medicare programs. read more

Inflation

Inflation is a decrease in the purchasing power of money, reflected in a general increase in the prices of goods and services in an economy. read more

Old-Age, Survivors, and Disability Insurance (OASDI) Program

The Old-Age, Survivors, and Disability Insurance (OASDI) program is the official name for Social Security in the United States. read more

Payroll Tax : Overview & Examples

A payroll tax is a percentage withheld from an employee's salary and paid to a government to fund public programs. Learn more about payroll taxes here. read more

Self-Employed Contributions Act (SECA) Tax

The Self-Employed Contributions Act (SECA) tax is a U.S. government levy on those who work for themselves, rather than for an outside company. read more

Social Security Act

The Social Security Act established a benefits system for people who are retired, jobless, or have a disability. A payroll tax funds these benefits. read more

Social Security Benefits

Social Security benefits are payments made to qualified retirees and disabled people, and to their spouses, children, and survivors. read more

Social Security Tax

This tax, levied on both employers and employees, funds Social Security and is collected in the form of a payroll tax or a self-employment tax. read more