Longtime Homebuyer Tax Credit

The longtime homebuyer tax credit was enacted by the government alongside other similar homebuyer tax credits, including the first-time homebuyer tax credit, to bring new buyers to the housing market. The purpose of the longtime homebuyer tax credit was to bring buyers to the housing market, alongside other tax credits, such as the first-time homebuyer tax credit. The longtime homebuyer tax credit was a federal income tax credit available to homebuyers who had owned and lived in the same principal residence for five of the last eight years before the purchase of their next home. The longtime homebuyer tax credit was a federal income tax credit available to homebuyers who had owned and lived in the same principal residence for five of the last eight years before purchasing their next home.

What Was the Longtime Homebuyer Tax Credit?

The longtime homebuyer tax credit was a federal income tax credit available to homebuyers who had owned and lived in the same principal residence for five of the last eight years before the purchase of their next home. In order to qualify for the credit, most homebuyers would have had to sign a binding sales contract for the home before April 30, 2010, and close on the purchase before June 30, 2010.

Understanding the Longtime Homebuyer Tax Credit

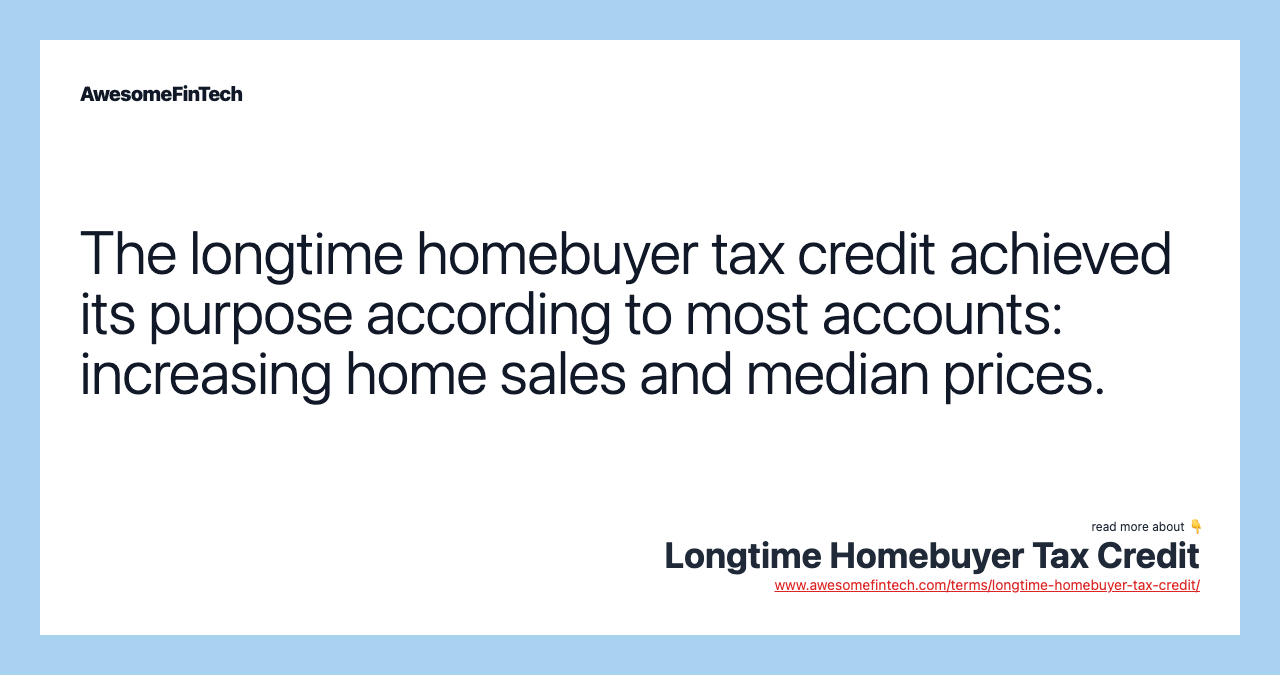

The longtime homebuyer tax credit was enacted by the government alongside other similar homebuyer tax credits, including the first-time homebuyer tax credit, to bring new buyers to the housing market. The government hoped the credits would increase demand and stabilize falling housing prices. By most accounts, the credits were successful in increasing home sales and median prices. Critics of the tax credit believe that this subsidy artificially inflated home prices and acted as only temporary support for falling prices.

The first-time homebuyer tax credit was a refundable tax credit made available to Americans purchasing their first home. The credit originally applied to home purchases made by qualified first-time buyers between April 9, 2008, and July 1, 2009. However, the Obama administration extended the original time frame requiring homeowners to have a signed sales contract until May 1, 2010, and gave them until the end of June 2010, to close the transaction.

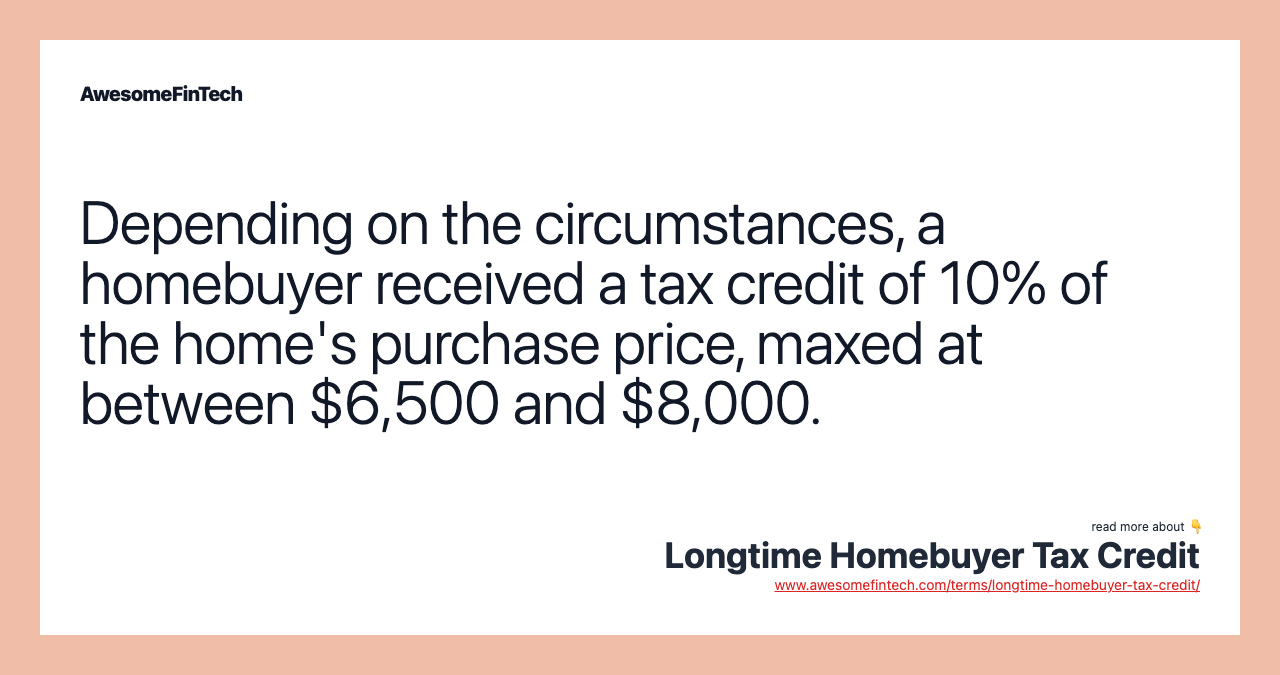

Beginning Nov. 7, 2009, long-time residents who owned their own homes also became eligible for the credit. The maximum credit for this group was $6,500, which, with some exceptions, did not have to be repaid. Long-time homeowners who bought a replacement home after Nov. 6, 2009, or in early 2010 may have been eligible to qualify for a credit of up to $6,500 under the rules.

Special Considerations

Under a special rule, long-time homeowners who bought a replacement home after Nov. 6, 2009, or in early 2010 may have qualified as well. To qualify as a long-time resident, taxpayers must have owned and used the same home as their principal residence for at least five consecutive years during a specified eight-year period.

If two people were buying a home together but were not married, the tax credit would only count for one individual. For example, both individuals would not be able to receive a tax credit of $6,500 for a total amount of $13,000. The tax credit for the home purchase would still just be $6,500. The credit, however, was meant to be split amongst all buyers. In addition, being a cosigner on another property did not preclude an individual from benefiting from the tax credit when they were able to make their own home purchase.

Though the longtime homebuyer tax credit has expired, there are other federal programs in place where homebuyers can benefit from tax credits. The Biden administration has also introduced a new tax credit bill for first-time homebuyers for up to 10% of the home's purchase price with a cap of $15,000.

Related terms:

Demand

Demand is an economic principle that describes consumer willingness to pay a price for a good or service. read more

First-Time Homebuyer Tax Credit

The federal first-time homebuyer tax credit was ended in 2010 but there are other state and federal programs designed to encourage homeownership. read more

First-Time Homebuyer

A first-time homebuyer is someone who is buying their first home. read more

First-Time Homebuyer Credit and Repayment of the Credit

Form 5405 is an IRS tax form filed by homeowners to claim a tax credit for a primary residence purchased between 2008 and 2010. read more

Miscellaneous Tax Credits

Miscellaneous tax credits are a group of tax credits that apply to taxpayers in specific situations. read more

Mortgage

A mortgage is a loan typically used to buy a home or other piece of real estate for which that property then serves as collateral. read more

National Housing Act

The National Housing Act, passed in 1934 to strengthen the residential real estate market, created the Federal Housing Administration (FHA). read more

Principal Residence

A principal residence is the main home that a person inhabits and uses for the majority of the time. read more

Refundable Credit

A refundable credit is a tax credit that can lower a taxpayer's tax liability regardless of the amount of that liability. read more